Research Notes

Strategy

- A key technical signal just flashed. The S&P 500's 50-day moving average crossed above its 200-day - triggering a golden cross.

- Since 1927, buying on this signal has outperformed buy-and-hold on a CAGR basis and delivered nearly 50% more Sharpe.

- Since 1927, buying on this signal has outperformed buy-and-hold on a CAGR basis and delivered nearly 50% more Sharpe.

- Last week, we flagged July as a seasonally strong month. That view just got reinforcement from a rare setup: a -20% drawdown in the first half. It's only happened 15 times since 1927, but when it does, July and August tend to rally.

- Sentiment is no longer at panic levels, but it's not euphoric either. Given the strength of the Q2 rally, we'd expect a bit more bullish conviction. That gap could be fuel - not friction - for the next leg.

- Global equities just made a new high, and beneath the surface, regional momentum is gaining traction.

- South Korea is a standout. After a strong leg higher, we'd welcome some consolidation - but the broader setup still points up.

- South Korea is a standout. After a strong leg higher, we'd welcome some consolidation - but the broader setup still points up.

- Financials continue to lead. Seasonality has their back, and the technicals remain constructive. Use pullbacks and sideways action to add exposure - this trend still has room to run.

Economics

- While June's headline jobs report surprised to the upside after ADP's negative print, looking deeper, we find the drop in unemployment from 4.3% to 4.1% stemmed largely from a 130k-person contraction in the labor force.

- Similarly, the household survey showed participation rate dropped to 62.3%, from 62.4% last month and 62.6% last year - a 130k drop MoM and down 745k from 2 months ago.

- Additionally, on the wage front, hourly earnings rose just 0.2% bringing yearly gain to 3.1%, well below the 3.8% from a year ago. This pairs with a shortened workweek to 34.2 hours from 34.3. As a result, average weekly earnings dropped.

- Just over 20% of outstanding mortgages were originated below 3%, a slight dip from 20.8% at the end of 2024. Loans in the 3-4% range have slipped to 32.7%, down steadily from over 35% earlier this year. The 4-5% cohort continues to decline, while 5-6% remains relatively flat.

- But the shift is happening on the margin: mortgages originated at 6% or higher now represent 18.8% of the market and continue to rise. It's a slow but persistent tightening of monetary conditions - and it's showing up in borrower behavior.

- But the shift is happening on the margin: mortgages originated at 6% or higher now represent 18.8% of the market and continue to rise. It's a slow but persistent tightening of monetary conditions - and it's showing up in borrower behavior.

- The May JOLTS report surprised to the upside, with private-sector job openings jumping by 374,000 - the second monthly increase in a row.

- But beneath the surface, the story narrows: 314,000 of those new openings came from accommodation and food services, marking the largest one-month increase (in percentage terms) since May 2020. It's a sharp move - and one that diverges from most other measures of labor demand.

- The total private sector job openings rate stood at 4.9%, the highest level since November. Taken at face value, this mitigates the risk of higher unemployment.

- That said, the more recent data points - including elevated continuing claims - imply the hiring rate may already be rolling over. The JOLTS data may reflect a temporary spike rather than a sustainable trend.

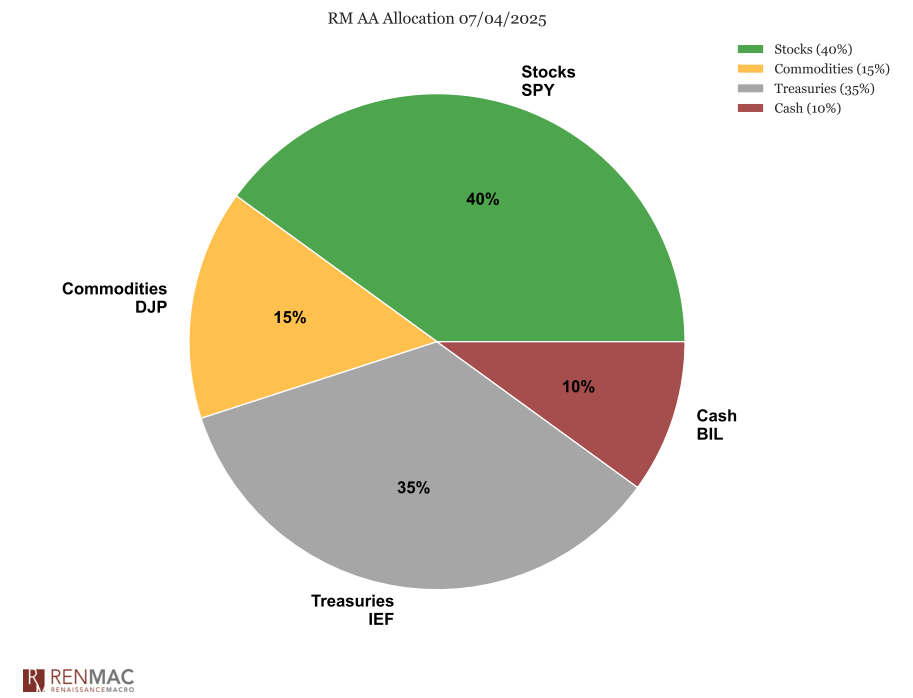

Asset Allocation Model

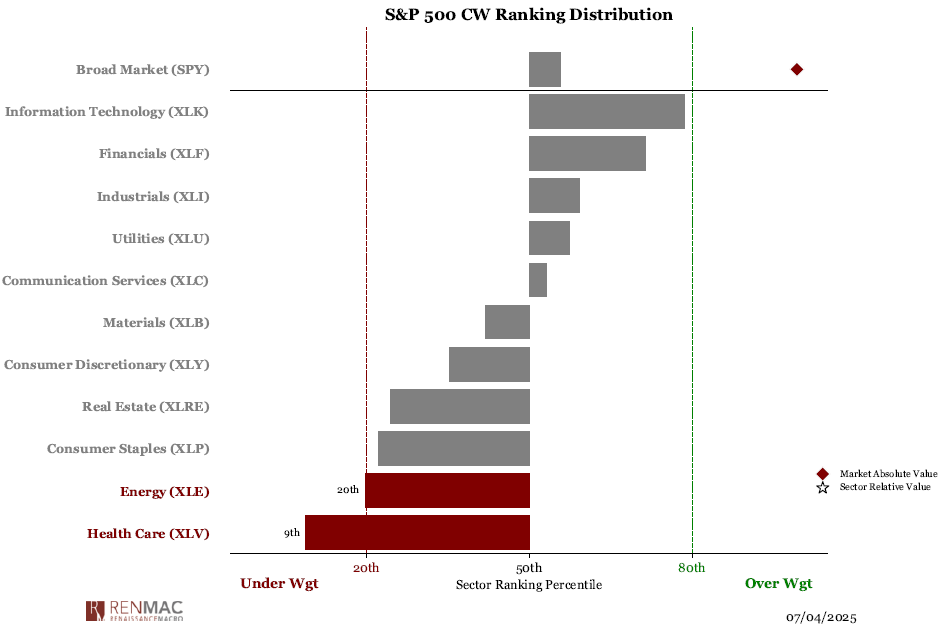

Sector Ranks

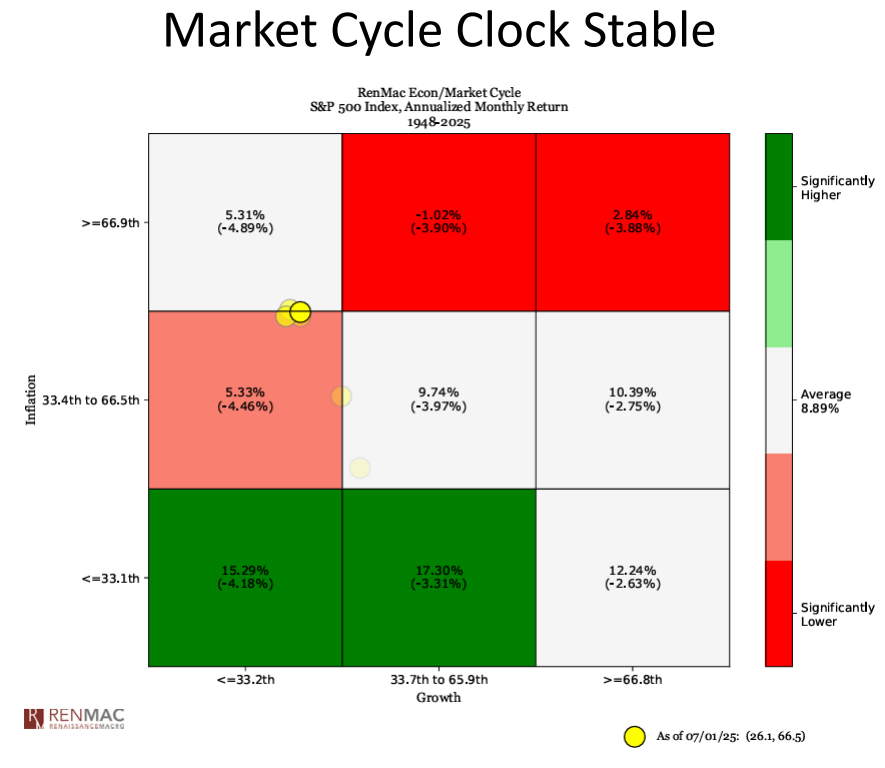

Sector Ranks  Chart of the weekThere is no discernable movement as we've been stuck in the same zone for the last four months. From a historical perspective, we know the clock tends to move down and to the left, then up and to the right. The path going forward tends to be better for the Fed and for rates with lower tenure yields.

Chart of the weekThere is no discernable movement as we've been stuck in the same zone for the last four months. From a historical perspective, we know the clock tends to move down and to the left, then up and to the right. The path going forward tends to be better for the Fed and for rates with lower tenure yields.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week