Research Notes

Strategy

- S&P 500 made a 65-day high Wednesday by poking through 5990 intra-day. It's a condition we use to help assess the underlying trend, and one some use in allocating dollars to uptrends or downtrends.

- The breakout, though soft, will have systematic investors adding to their stock allocations creating an additional source of demand.

- The breakout, though soft, will have systematic investors adding to their stock allocations creating an additional source of demand.

- Sell in May is a myth. May tends to be a flat month for SPX returns, but it's the next 3 months that tell a different, more bullish, story than conventional wisdom implies.

- In case you missed it, here is a video from deGraaf's WSG explaining this.

- In case you missed it, here is a video from deGraaf's WSG explaining this.

- Stick with our call towards high momentum stocks. Relative performance leaders today are the narratives for tomorrow. Seasonality confirms this call as June, July, August, and September, momentum tends to work.

- Tech has rallied with beta trade, but not all tech looks the same. XLC made fresh 65-day high Thursday, but Semi's tell a different story - stay with the best charts, but don't get swept off your feet after this beta bounce.

- Excess optimism in Tesla showed its teeth Thursday as one of the most predictable divorces in history occurred. We're looking for a deeper oversold condition to develop, and see TSLA as vulnerable to $220.

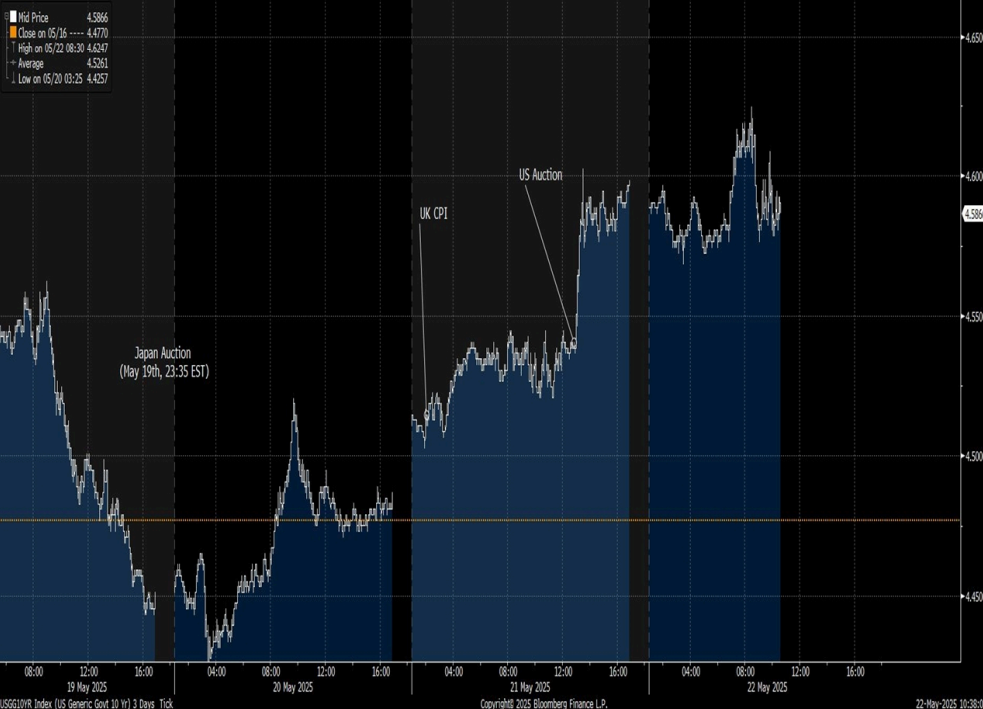

- We've seen some contraction in yields, but nothing meaningful takes place at this point unless/until we breakout 4.20% on the downside or 4.60% on the upside. Until then, we're neutral with a small bias to higher yields.

- Good things tend to happen to Bitcoin when there's excessive long positions by commercials. Winner 89% of the time over the next 13 weeks when this triggers.

Economics

- NFP came in at 139k, slightly ahead of expectations. With that being said, revisions were notable and negative. Previous months revised down by 95k.

- So far this year, NFP has been averaging 124k compared to 168k for same period last year.

- So far this year, NFP has been averaging 124k compared to 168k for same period last year.

- On the flip side, Household Survey showed full-time workers decreasing by over 600k, while part-time barely ticked up, telling us a different story.

- The Fed and the markets appear to be looking at labor market conditions at a surface level while ignoring some obvious signs of weakness under the surface.

- Labor market is slacking, even if we're not seeing it in NFP quite yet. ADP employment rose just 37k in May. Last 3 months see an average of just 81k, the weakest in two years.

- Interestingly, ADP shows weakness in education & health services, at odds with the message from BLS data.

- Interestingly, ADP shows weakness in education & health services, at odds with the message from BLS data.

- Home prices declining as inventories climb, and labor conditions cool down. This is a bad combination, especially considering the Fed's wait and see approach.

- Redfin recently reported there are 33.7% more sellers than buyers. At no other point in records dating back to 2013 have sellers outnumbered buyers by this large of a number.

- Redfin recently reported there are 33.7% more sellers than buyers. At no other point in records dating back to 2013 have sellers outnumbered buyers by this large of a number.

- ISM Services PMI fell sharply to 49.9 in May, driven by significant decline in new orders, both at their weakest levels since June 2024.

- Business activity index weakened considerably, and prices-paid index surged to 68.7, it's highest reading in 5 years - indicating escalating cost pressures due to tariffs.

- This report paints a picture of a services sector struggling under the weight of higher tariffs and weakening demand.

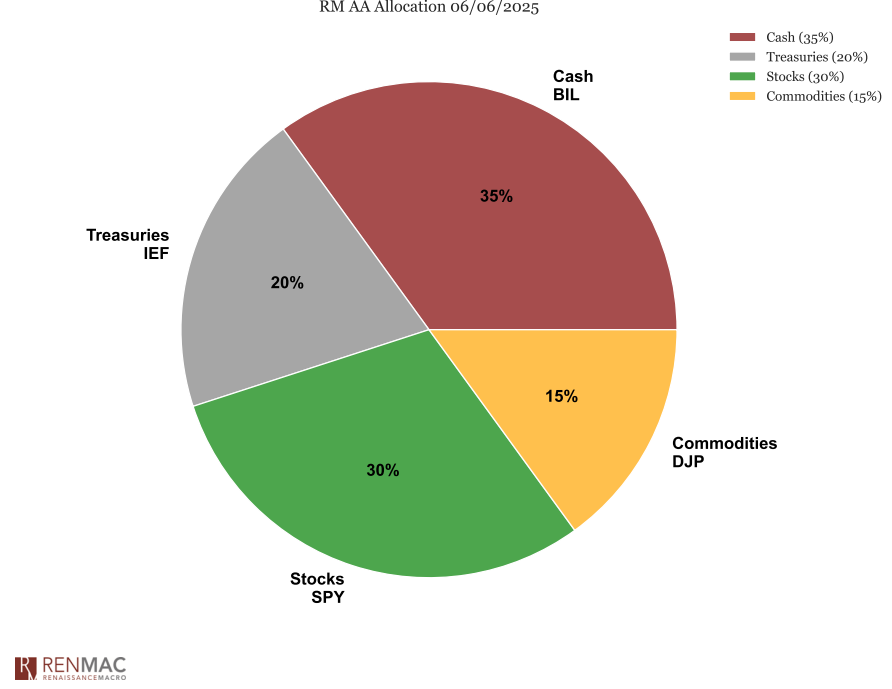

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the weekWith growth in the 24th and inflation in the 66th percentiles, S&P returns remain choppy. Tariff uncertainty mimics a supply shock. Bullish forces persist but are muted. Resistance at 6150, support at 5700. See video from deGraaf on the Market Cycle Clock here.

Chart of the weekWith growth in the 24th and inflation in the 66th percentiles, S&P returns remain choppy. Tariff uncertainty mimics a supply shock. Bullish forces persist but are muted. Resistance at 6150, support at 5700. See video from deGraaf on the Market Cycle Clock here.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week