Research Notes

Strategy

- We had a significant shift in our Asset Allocation model this week. Here is a video from Jeff deGraaf explaining why.

- We find ourselves in familiar territory this month - caught in the same overbought conditions that emerged earlier. But here's what makes this interesting: this isn't signaling trouble Ahead. Instead, we're witnessing a classic consolidation pattern that typically resolves through time rather than dramatic price swings, and that's precisely the script markets are following.

- Something fundamental has shifted in market dynamics. Yields have moved from supporting actor to center stage, now explaining roughly 60% of equity movements - nearly double their historical influence of 30-40%.

- The 30-year is consolidating right at resistance levels, while real yields are beginning to flex their competitive muscle.

- When bonds start offering compelling returns with seemingly lower risk, the great rotation of capital becomes more than just market chatter.

- Oil's overbought condition is rippling through energy names across the S&P 500, creating a classic tug-of-war between strong underlying trends and stretched valuations.

- Meanwhile, European defense spending commitments are quietly reshaping the Aerospace & Defense landscape, pushing these names higher and creating a golden cross in the Industrials ETF (XLI) that few are talking about.

- The real surprise? Financials are stealing the show. Investment banks and brokers are quietly notching new relative strength highs while most attention focuses elsewhere.

- The Bloomberg Commodity Index sits on the verge of what could be a significant breakout from a large base formation. Precious metals are doing their part, energy's recent surge is contributing, and a handful of other commodities are building momentum behind the scenes.

- Keep one eye on the Yen moving forward. Its inverse relationship with broader markets isn't a bearish call - it's simply one of those correlations that tends to matter when it matters most.

Economics

- While markets parsed every word from Powell's latest appearance, Neil Dutta sees through what many interpreted as dovish signals.

- The Fed's Summary of Economic Projections tells a different story - unemployment revised up by 0.1%, core inflation bumped higher by 0.3%. Run these numbers through a standard Taylor Rule model, and the implied Fed Funds rate remains essentially unchanged. Sometimes the most important Fed communication happens in the footnotes, not the headlines.

- Here's where the disconnect gets interesting. Powell described labor market conditions as "solid", but Dutta's reading of the data suggests a different reality is emerging. The Fed Chairman also highlighted that "economic activity has continued to expand at a solid pace", yet economic data surprises have been pointing in one direction: unambiguously negative.

- After Governor Waller's Friday morning CNBC appearance, Dutta made a bold call: Waller should be the next Fed Chairman. While the broader FOMC maintains its "wait to learn" stance, Waller is already conducting the scenario analysis that everyone claims to want but few are actually doing. Sometimes leadership reveals itself in the approach, not just the position.

- The housing market story continues to unfold in ways that may surprise those focused on headline price movements. The NAHB Housing Market Index collapsed to 32 in June - the lowest reading since 2022.

- For builders, the economics are becoming increasingly challenging: rising resale inventories are pressuring prices, forcing builders to offer substantial incentives just to move inventory. When the people who build homes for a living are struggling to sell them, it's worth paying attention.

- For builders, the economics are becoming increasingly challenging: rising resale inventories are pressuring prices, forcing builders to offer substantial incentives just to move inventory. When the people who build homes for a living are struggling to sell them, it's worth paying attention.

- Perhaps most telling are the Worker Adjustment and Retraining Notifications (WARN) - those 60-day advance notices companies must file before layoffs. This leading indicator has quietly climbed to its highest level since August 2023. In the world of economic data, few things are more forward-looking than a company's decision to formally prepare for workforce reductions.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

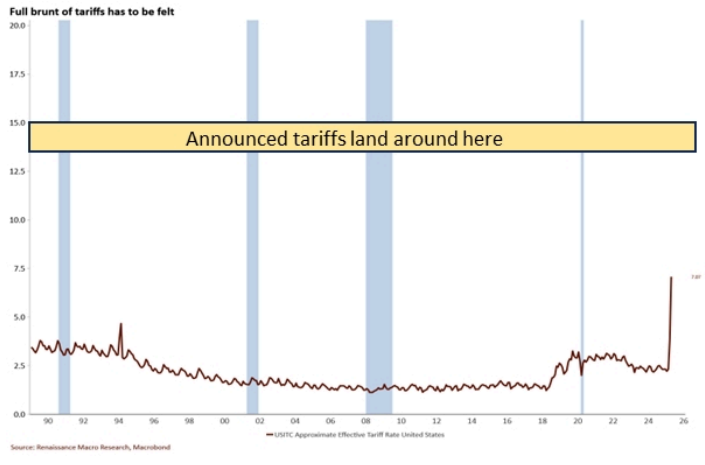

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

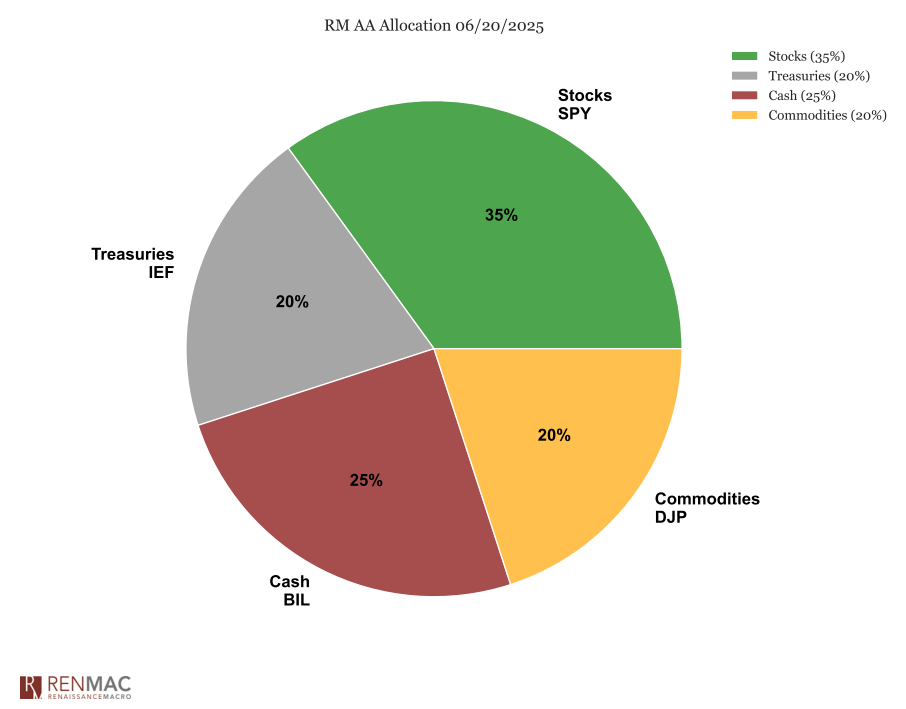

Asset Allocation Model

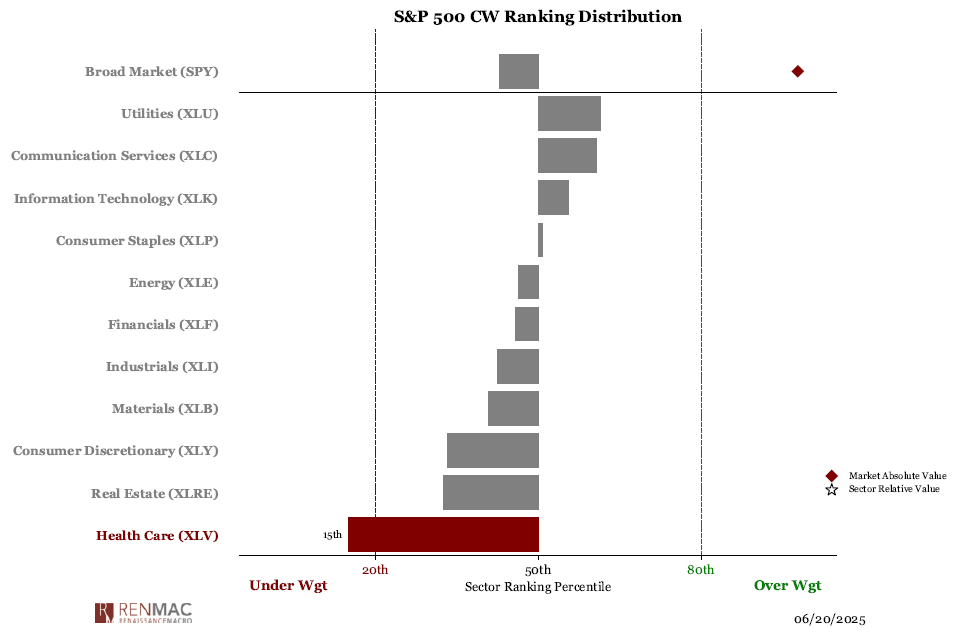

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week