Research Notes

Strategy

- We're entering July with a familiar setup - one that's historically kind to equities. July tends to be the strongest month of the year, and with yields typically easing through Q3, the stage is quietly being set for relief.

- The S&P has now retraced nearly all of its April drawdown, rising 27% in a sharp V-bottom move that's pushing right up against February's highs.

- Yet despite the rally, sentiment hasn't caught up. The latest II survey still shows bull - a contrarian fuel source markets love to burn through.

- Under the surface, just 6% of S&P 500 stocks are hitting 52-week highs - this can and usually does improve as the market makes a new high, so we're giving it some rope. Encouragingly in our momentum models, financials are well represented. Momentum and relative strength remain the best filters in this phase.

- Seasonality agrees. Q3 is typically when momentum takes the wheel - especially three months off a major low. That handoff is happening now.

- Meanwhile, the dollar just slipped to a multi-year low. DXY is nearing long-term uptrend support near 96.50, and while a bounce is possible, the path of least resistance remains lower, though Jeff does see high real-yields as a reflection of buyers strike foreign governments are using to protest tariff noise. Capital eventually flows to where it is treated best.

- Bitcoin continues to consolidate in lockstep with equities, and with the broader market knocking on breakout levels, the setup for a move higher is materializing.

- Tech is making the case for leadership again. XLK just posted a new high - both in absolute and relative terms - Semis are not leadership in our work, but NVDA's breakout reinforces the selected opportunities in this sub-industry.

Economics

- Housing data is sending a clear signal: the freeze is thawing, but only slightly. Existing home sales held steady at 4.03 million SAAR in May - flat since March - but inventory is on the rise, now at its highest level since mid-2020. That 20% YoY jump in supply is finally cooling prices, which are down 2.6% annualized over the past six months. Consumers, however, aren't feeling much relief.

- June's Conference Board Consumer Confidence Index fell to 93, well positioned below expectations. The disconnect? Labor. Despite headlines calling conditions "solid", households don't seem to agree.

- The Labor Differential - a key subcomponent tracking whether people think jobs are plentiful - just hit its worst level since the pandemic. The decline wasn't about more people saying jobs are hard to get: it was about fewer saying they're easier to find.

- The dynamic hasn't changed: low hiring, low firing. If you're employed, you're fine. if you're looking, not so much. In this environment, it doesn't take many layoffs to tip jobs growth negative.

- The Fed, for now, seems unbothered. At the margin, fewer FOMC participants see upside as risk in labor. Whether that's optimism or denial remains to be seen.

- Inflation expectations are holding steady - unless you ask UMich. While the NY Fed and Atlanta Fed data show relative calm, the UMich survey stands out: a sharp rise in the share of respondents expecting prices to jump 10% or more is hard to ignore.

- On the corporate side, business investment remains sluggish. AI capex is doing the heavy lifting, but it's not broad-based.

- Non-residential structures investment continues to cool. Even with trade tensions easing, capital spending intentions haven't picked up. Less uncertainty hasn't translated to more optimism.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

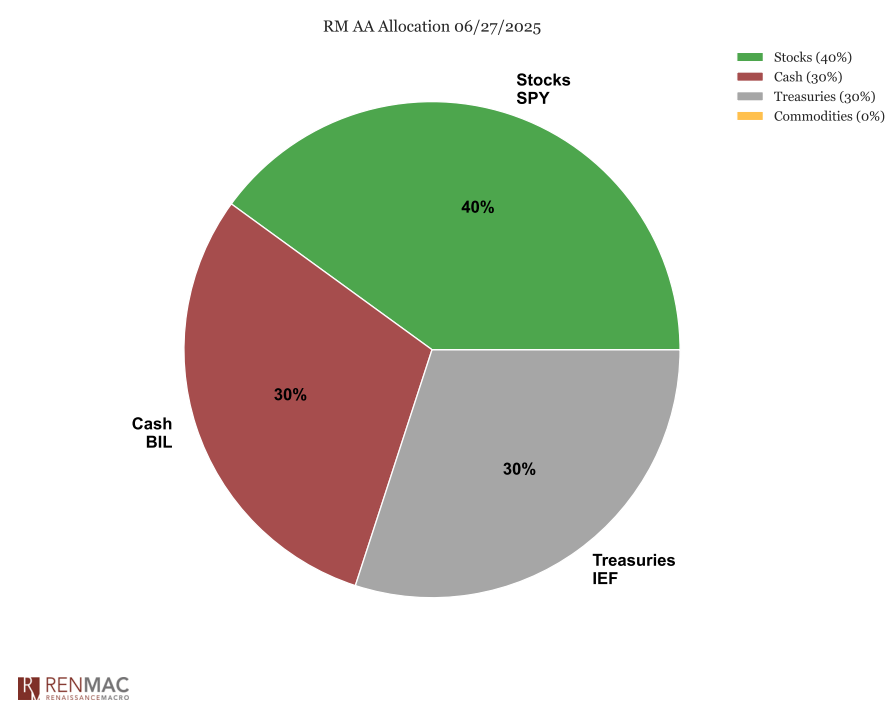

Asset Allocation Model

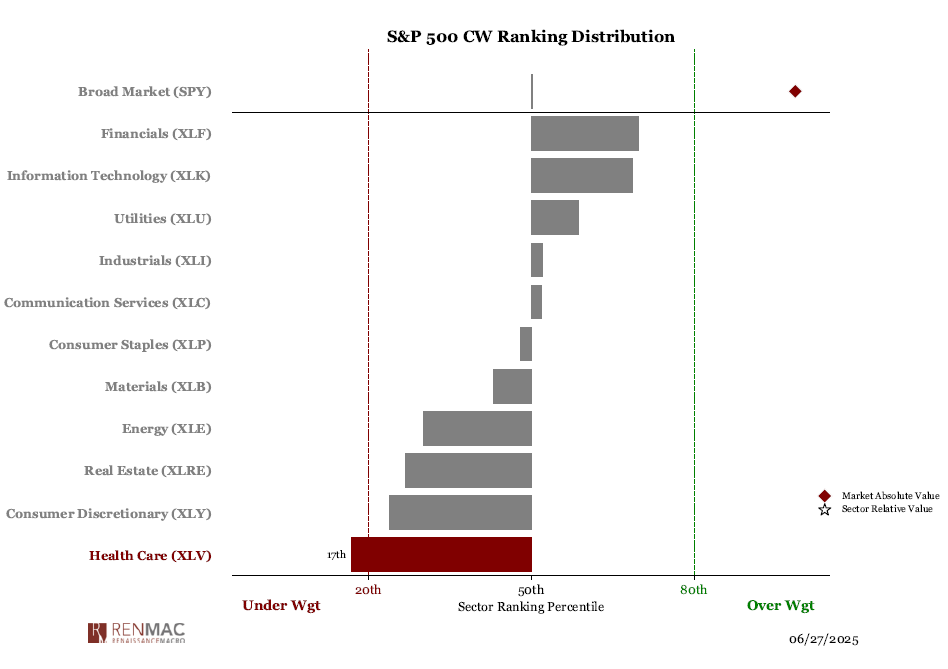

Sector Ranks

Sector Ranks  Chart of the week

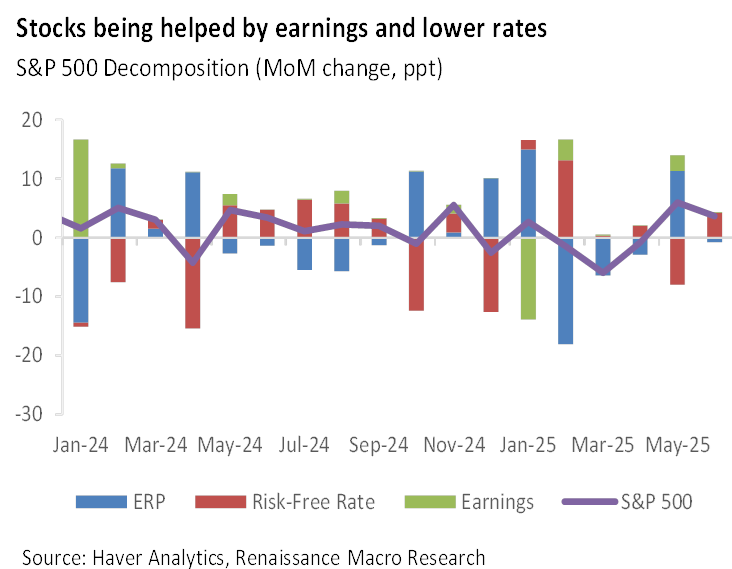

Chart of the week