Research Notes

Economics

- Durable goods orders surged in March by 9.2%. On the flip side, six-month capex intentions have collapsed. Expect core durables to soften in Q2.

- Neil believes that while tariffs will raise the price for consumer goods, service sector inflation will continue to slow. Inflation expectations have been a reason for the Fed to hold off on rate cuts. This would undercut it.

- Recent reports indicate Trump may lower China tariffs to about 50%. A couple observations from Neil here:

- Goods are not moving at the current rates, and the administration has said it does not want a full decoupling.

- If households see the tariffs as likely to drop in the future, they will spend less today.

- Dutta says this only serves to increase the fog in the high-frequency data and he's not sure why any of this is "good".

- New home sales rose 7.4% in March, ahead of expectations, however due to increase in rates early this month, we expect new home sales to moderate in the next few months.

- Powell recently noted the disconnect between hard and soft, or survey-based, measures of economic data. Our work confirms the disconnect between hard and soft data.

- Soft data composite index has collapsed in recent months, while hard data composite index has improved of late.

- Consumers and businesses pulling forward activity in anticipation of tariffs is likely a major cause of this disconnect.

- Prior to tariff news, hard-data was already slowing notably.

- Jeff has been calling out for a few months now that he likes ACWI ex US, Neil is now hopping on that as well saying he prefers to be in Europe since tariffs won't impact consumers there, and ECB is likely to continue cutting while the US has higher neutral rate (r-star).

Strategy

- The market is back at resistance, having retraced half of the sell-off. deGraaf thinks the extreme sentiment can push us to ~5700, but the lack of momentum we're seeing in the rally limits the upside. We understand the risk/reward is not great, but you don’t want to be chasing as the market gets overbought.

- Owning high-beta names is still one of our favorites. Recent movement in Semi's is a good reason why. The group is still in a bearish trend, but look for some more upside before fading.

- Sellers frenzy in Semiconductors and buyer's frenzy in Consumer Stapes. This coincides with our call to move toward high beta names.

- Sellers frenzy in Semiconductors and buyer's frenzy in Consumer Stapes. This coincides with our call to move toward high beta names.

- Dollar bouncing off deep oversold condition. Consensus Inc data shows excessive bullish sentiment in other currencies which is supportive of our USD call.

- Look for a further correction in gold and gold miners, however if we see any oversold conditions we would be buyers there.

- Bitcoin breaking out again. Typically moves in unison with the NDX.

- Energy outflows are accelerating, and momentum is fading as relative weakness persists. These metrics are indicative of a bottom forming, but we aren't there yet. We see most opportunities in tactical plays.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

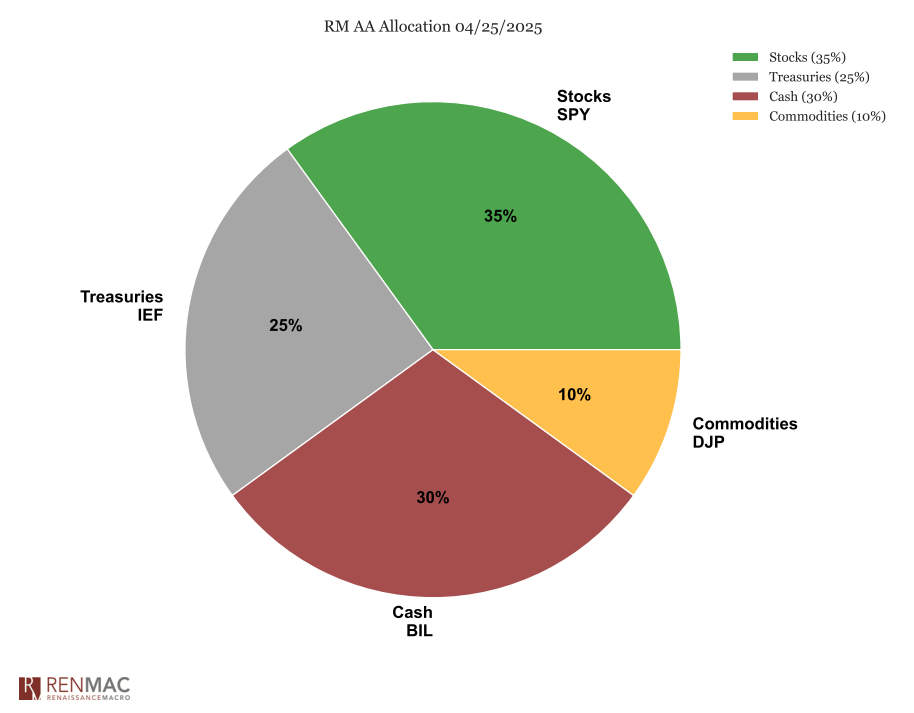

Asset Allocation Model

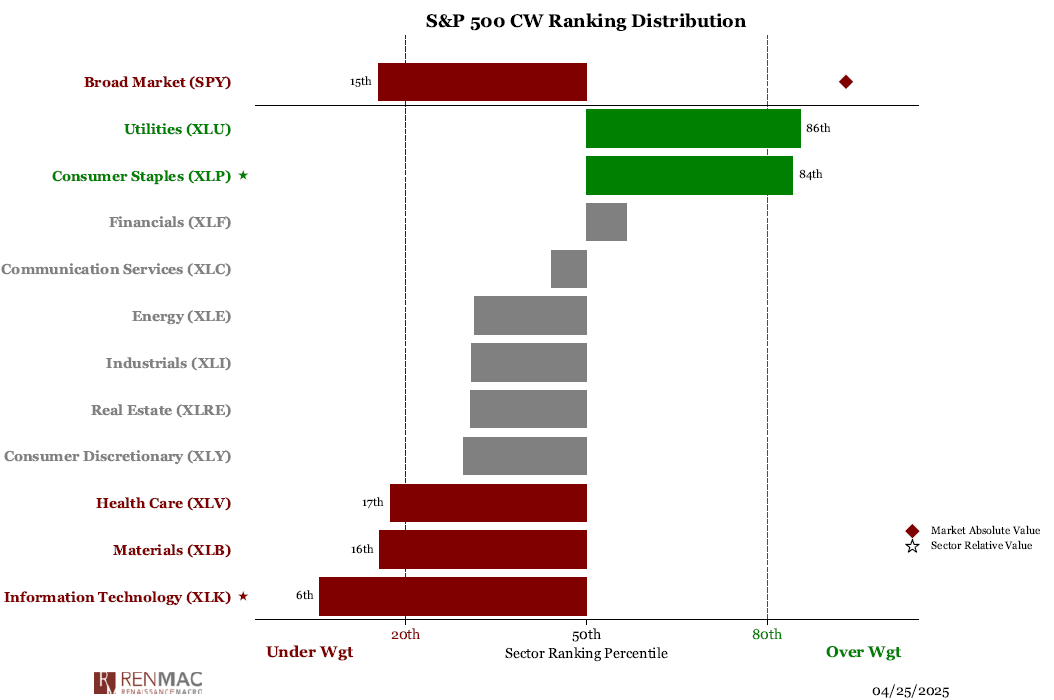

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week